Key Takeaways

- Regulators classify an inability to produce training records as a documentation deficiency, regardless of the technical reason.

- Day-1 examiner requests include completion records, assignment timestamps, assessment results, onboarding records, and third-party training documentation.

- An LMS outage during an active examination triggers 4 consequences: extended duration, a deficiency finding, expanded scope, and remediation tracked across future cycles.

- Adequate documentation has 4 attributes: completeness, timeliness, specificity, and retrievability, and retrievability is where platform reliability meets compliance standing.

- A compliance training platform should meet 4 reliability standards on examination morning, not just in normal operating conditions.

On the first morning of a regulatory examination, a Federal Deposit Insurance Corporation (FDIC) examiner opens a standard request list that includes completion records for Bank Secrecy Act/anti-money laundering/countering the financing of terrorism (BSA/AML/CFT) training, refresher courses on unfair, deceptive, or abusive acts or practices (UDAAP), and role-based onboarding curricula for consumer-facing staff. Your compliance officer opens the learning management system (LMS). The page does not load.

Regulators classify an inability to produce records as a documentation deficiency, regardless of the technical reason. A cloud-based LMS failure during an active examination triggers the same consequences as missing records, and those consequences persist well beyond the examination date.

Examination readiness is testable before the examiner arrives. This article runs the test: what examiners request on day 1, the 4 consequences when the system cannot answer, what adequate documentation requires, and the 4 reliability standards that decide whether your LMS passes. Getting all four right is what separates a merely functional LMS from a true AML compliance training platform.

What Banking Examiners Request on Day 1

Banking regulators conducting examinations under the Office of the Comptroller of the Currency (OCC), FDIC, National Credit Union Administration (NCUA), or Federal Reserve framework issue a pre-examination request list that typically includes training documentation. Those records function as primary evidence that the bank met its compliance obligations during the period under review, and examiners expect to access them quickly.

On day 1, examiners commonly request:

- Completion records for mandatory courses: BSA/AML/CFT fundamentals, including Customer Due Diligence (CDD) content governed by existing CDD program requirements, UDAAP, the Truth in Lending Act (TILA), and the Community Reinvestment Act (CRA). The Financial Crimes Enforcement Network’s (FinCEN) April 2026 proposed rule would restructure AML/CFT program requirements; it superseded the 2024 program proposal and remains in rulemaking as of mid-2026.

- Assignment timestamps showing when training was distributed to each employee role

- Assessment results for employees who required remediation before certification

- New hire onboarding records for staff who joined during the examination period

- Vendor and third-party training records for functions covered under the 2023 Interagency Guidance on Third-Party Relationships (OCC Bulletin 2023-17)

These records must be tied to specific employees, specific courses, and specific dates. A spreadsheet reconstructed after the fact rarely satisfies an examiner, and a verbal assurance that the training occurred satisfies no one.

4 Consequences of a Cloud-Based LMS Outage During an Active Examination

A cloud-based LMS that becomes unavailable during an active examination does not create a grace period. The examination timeline continues, and each hour the records remain inaccessible adds complexity to the institution’s compliance response.

Consequence 1: Extended Examination Duration

When examiners cannot obtain documentation on the first request, they issue follow-up requests that extend the examination window and increase the cost of the engagement for the institution.

Consequence 2: Documentation Deficiencies in the Examination Report

Regulators distinguish between training that occurred without adequate documentation and training that simply did not occur, but from a documentation standpoint, both produce the same examination outcome.

Consequence 3: Expanded Scope in Adjacent Compliance Areas

Examiners who find incomplete BSA/AML/CFT training records typically look more closely at UDAAP procedures, CRA activity records, and other documentation-dependent compliance functions.

Consequence 4: Remediation Requirements That Outlast the Examination

When an examination report cites a documentation deficiency, the bank must provide a written remediation plan tracked in subsequent examination cycles. A single LMS outage during one examination can generate compliance overhead that persists for 2 to 3 examination periods.

What Counts as Adequate Compliance Training Documentation

Federal banking regulators do not prescribe a software platform. They prescribe outcomes: evidence that specific employees received required training within defined intervals and demonstrated sufficient understanding to proceed in their compliance roles.

The Regulatory Baseline

The Federal Financial Institutions Examination Council (FFIEC) BSA/AML Examination Manual sets the AML BSA training requirements examiners use to guide examinations at all federal banking agencies. It directs examiners to assess whether the bank maintains a written training program and whether management actively tracks completion, with documentation that identifies the subject matter covered, the employees who participated, and the date the training was provided.

The 2023 Interagency Guidance on Third-Party Relationships (OCC Bulletin 2023-17, jointly issued by the OCC, FDIC, and Federal Reserve) extends documentation expectations to vendor and third-party relationships. Banks that rely on vendors for compliance-covered functions are expected to oversee and document those relationships, including, where applicable, how the people performing covered functions are trained.

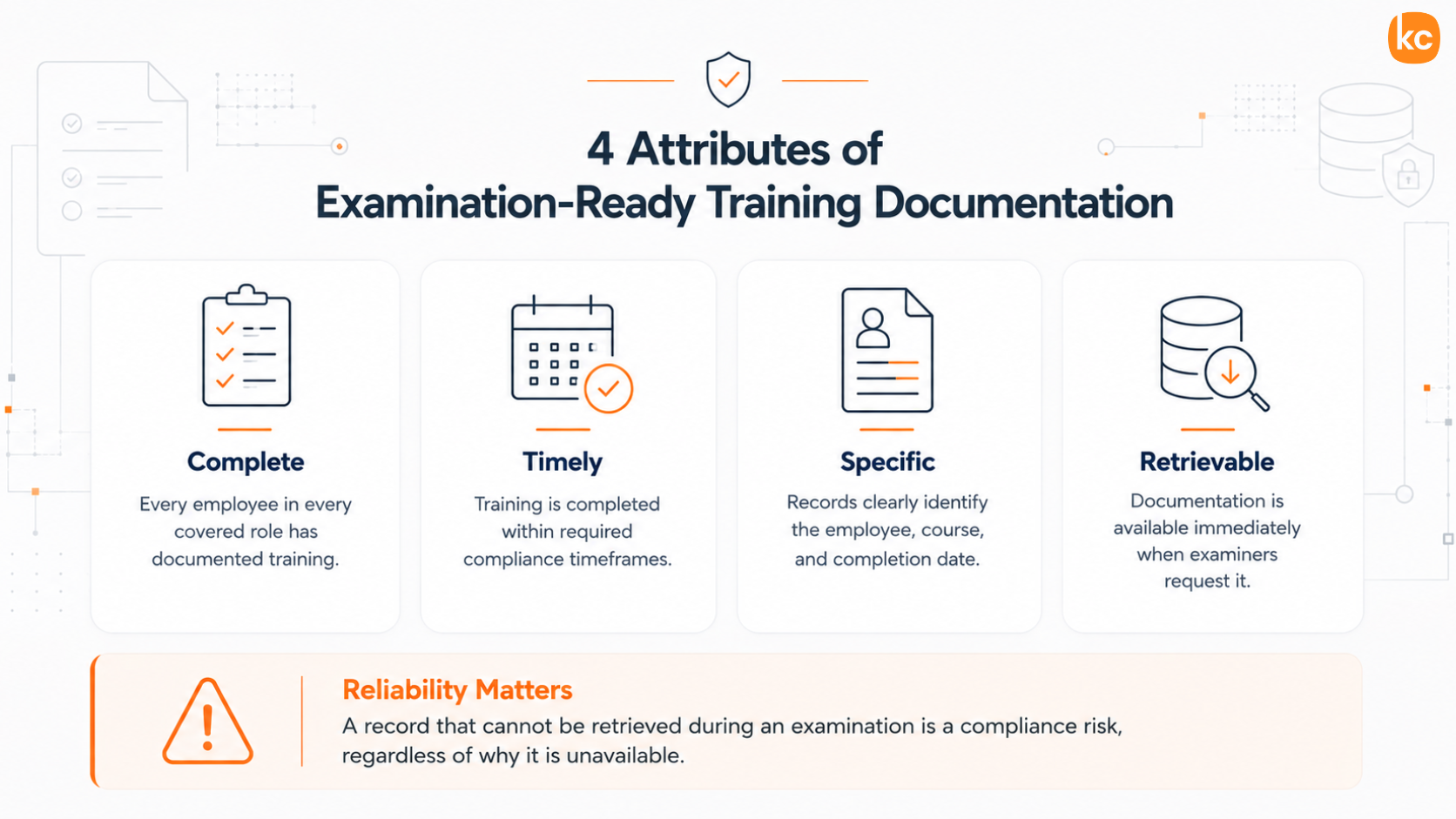

The 4 Attributes of Adequate Documentation

- Completeness: records cover all employees in covered roles

- Timeliness: records reflect training completed within required windows

- Specificity: records identify the course, the employee, and the date

- Retrievability: records can be produced on demand during an active examination

The last attribute is where technology reliability intersects directly with a bank’s compliance standing.

The Reliability Standards a Compliance Training Platform Must Meet

Banking institutions that deploy a cloud-based LMS for compliance training should verify that the platform meets the specific reliability requirements that examination conditions impose. A system adequate for general employee onboarding may fall short at 8 a.m. on an examination morning.

Examination readiness depends on the platform’s ability to meet 4 requirements simultaneously, not just in normal operating conditions but on the morning an examiner asks for the records:

- Contractual uptime: a minimum service-level agreement (SLA) of 99.9% for compliance-critical infrastructure. Downtime during an examination window produces the same outcome as a missing record.

- Same-day record export: examiners expect records to be exported promptly. A platform that cannot produce completion reports in structured CSV or PDF format within minutes is not suited for active examination conditions.

- Role-separated access: compliance officers need a reporting view that allows them to respond to examiner requests without exposing administrative controls or unrelated employee data.

- Immutable audit logs: all training activity should be logged with timestamps that cannot be edited. Examiners who question the integrity of training records will look for this evidence specifically.

How KnowledgeCity Builds Examination Readiness

Banking institutions manage compliance training obligations across OCC examination cycles, FDIC examinations, and NCUA supervisory reviews on a multi-year continuum, and the records generated by each training event must be as durable as the examination process that evaluates them.

KC Library carries role-based AML/BSA/KYC training organized as a training matrix per job code, with annual recertifications auto-assigned and tracked through KC LMS. Each completion generates a certificate linked to the employee’s record and stored as a timestamped, exportable training record: exam-ready completion records for every employee, every cycle. For the broader mandatory-course map (UDAAP, TILA, CRA, and consumer protection), ask the KnowledgeCity team during a working session which titles map to your institution’s specific requirements.

Real-time reporting lets compliance officers run completion queries by employee, department, role, or date range at any moment. When an examiner submits a documentation request, those reports export within minutes rather than after a reconstruction project.

Walk into the examination with the records ready. Exam-ready completion records for every employee, every cycle, exportable the morning the request list arrives.

Frequently Asked Questions

- What happens if a bank cannot produce training records during a regulatory examination?

Regulators classify an inability to produce records as a documentation deficiency, which is noted in the formal examination report. A written remediation plan must then be submitted and tracked in subsequent examination cycles. Findings of this type don’t close at the end of the current examination.

- What training courses do banking regulators most commonly request records for?

BSA/AML/CFT training is the most frequently requested topic, followed by UDAAP, TILA, CRA, and consumer protection. Examiners also commonly request records of new-hire onboarding and remediation courses completed by employees who did not pass initial assessments.

- Does a cloud-based LMS outage affect a bank’s examination outcome?

Yes. Regulators cannot distinguish between records that do not exist and records that exist in an inaccessible system. An LMS outage during an active examination can result in the same documentation-deficiency finding as a gap in the training program itself.

- How long do banking regulators typically review training records?

OCC and FDIC examinations typically review training records covering the 12 to 24 months preceding the examination date. Banks should maintain accessible training records for at least 36 months to cover the standard examination scope and allow for any targeted follow-up reviews.

References

- Federal Financial Institutions Examination Council. BSA/AML Examination Manual.

- Office of the Comptroller of the Currency, Federal Deposit Insurance Corporation, and Board of Governors of the Federal Reserve System. OCC Bulletin 2023-17: Interagency Guidance on Third-Party Relationships: Risk Management.

- Financial Crimes Enforcement Network. Anti-Money Laundering and Countering the Financing of Terrorism Programs, proposed rule, April 10, 2026 (Doc. No. 2026-07033).

- Federal Deposit Insurance Corporation. Risk Management Manual of Examination Policies.

- Office of the Comptroller of the Currency. Comptroller’s Handbook.